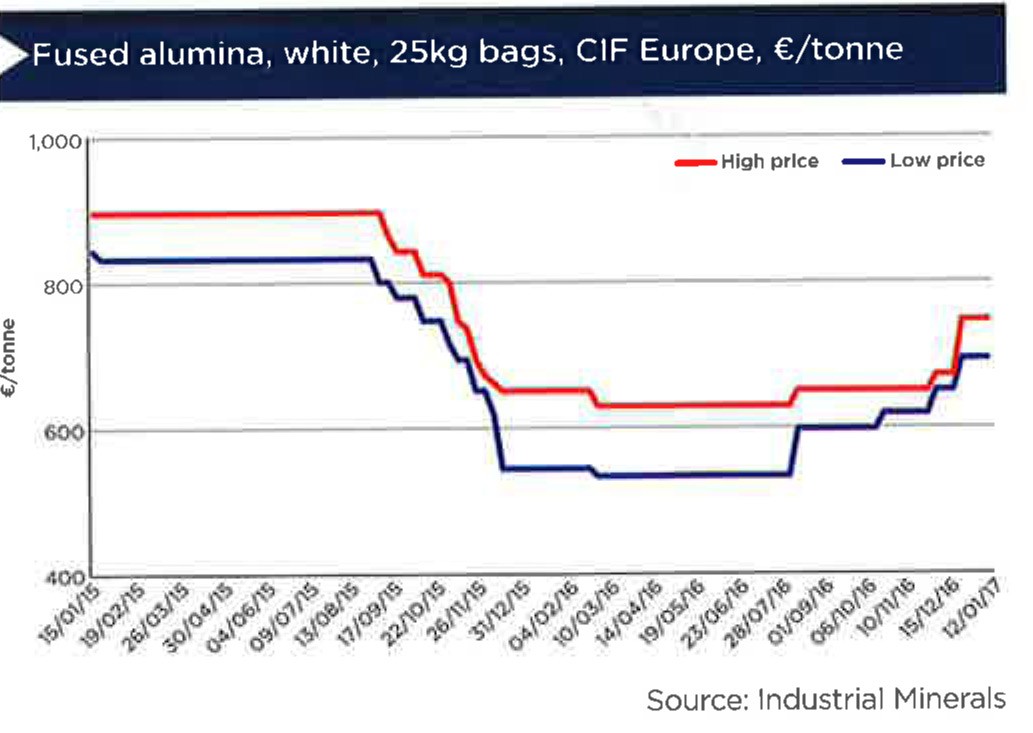

White fused alumina spot prices rose amid higher raw material cost, but increases in China are steeper compared with elsewhere as continuing environmental pressure restricted output amid stronger domestic demand.

Spiralling raw material cost is lifting white fused alumina (WFA) spot prices as Chinese producers raised their offers, market sources told IM.

Alumina is the key raw material used to produce WFA, and recent restocking from Chinese aluminium smelters have pushed prices up by about 40% since October.

Chinese domestic alumina prices was assessed at a range of 2,700-2,850 yuan ($390-412)/tonne on a delivered in China basis, up from 2,650-2,800 yuan a week earlier, according to IM’s sister publication Metal Bulletin on Thursday November 24.

Driven by the uptrend in China, alumina prices elsewhere in the world is also rising. Inferred alumina index on a FOB Brazil basis, the reference for European smelters, was calculated at $318.47/dry metric ton, up $17.02/ton compared to a fortnight ago, according to Metal Bulletin this week.

As smelters’ alumina purchased volume are often much bigger compared with WFA producers, with the average standard cargo size at 30,000-35,000 tonnes, the former could secure lower volume-related prices.

One WFA producer in China has quoted alumina prices as high as 3,000 yuan ($433.50)/tonne, and he had to raise his WFA offers to reflect higher raw material and production cost.

Spot refractory-grade WFA (99.0% Al2O3 min, in 25kg bags) prices were assessed at €650-680/tonne on a CIF Europe basis, up €27.50/tonne compared with the previous week, according to IM’s assessment on 24 November.

Materials for spot delivery in Germany traded in the region of €680/tonne on a DAP basis, one Europe-based producer told IM.

Stronger demand, reduced supply in China

Due to the Chinese government’s anti-pollution crackdown on many production facilities in China since July, many fused-alumina plants that did not meet environmental standards were shut down. The shut down were particularly severe in Henan province, one of the main regions for fused-alumina production.

As a result, reduced WFA supply amid firm domestic demand is supporting prices in China, producers in the country said.

Chinese-origin WFA were trading in the region of 5,000 yuan (€682.45)/tonne on an ex-work basis within China, according to two suppliers.

Many expect strict anti-pollution checks to remain in China for the long-term, and consequently, the restricted production is expected to support WFA prices in the country.

In contrast, WFA supply in Europe were not disrupted and the region remained well-supplied amid weak refractory demand. Consequently, European product prices did not receive the strong boost like its Chinese counterpart.

China is one of the biggest fused alumina producer in the world.